What Is Money?

Then suddenly, with grokking so blinding that he trembled, he understood money. These pretty pictures and bright medallions were not "money"; they were symbols for an idea which spread through these people, all through their world. But things were not money.... Money was an idea.... The flow and change and countermarching of symbols was beautiful in small..., but it was the totality that dazzled him, an entire world reflected in one dynamic symbol structure. Mike then grokked that the Old Ones of this race were very old indeed to have composed such beauty....

- Robert Heinlein, Stranger in a Strange Land

To understand money, let's start in 1933.

In 1933, the U.S. was in the middle of the Great Depression. Gold was money, and money (theoretically) was gold. Indeed, the face of the $10 bill used to say, “Will pay to the bearer on demand ten dollars” and “This note . . . is redeemable in lawful money at the United States Treasury or at any Federal Reserve Bank.” Until 1933, you could walk into a Federal Reserve Bank, plop down $20.67 in cash, and demand an ounce of gold.

But this simple account doesn't tell the whole story. In 1933, at $20.67 per ounce, the U.S. had roughly $4.3 billion of gold reserves. But it had about $5.3 billion of currency in circulation. The U.S. government could print or mint its own currency, so there's no reason it could not print more money than it was theoretically capable of redeeming. As long as there was not a wholesale flight to gold, and as long as people had faith in the U.S. government, this was not a problem.

But even this doesn't tell the whole story. If you totaled up all of the money Americans said they had in their bank accounts, you'd get a number closer to $40 billion, which meant in some ways that each ounce of gold was "claimed" by roughly 10 people. How was there so much wealth based on so little gold?

The Money Flow

If I deposit $20 in Chase Bank, I'm lending the bank $20 of my money, and Chase is giving me a $20 "IOU," which we call a demand deposit. If I go to the store and write a check for $20, I'm not actually giving the store "money," per se; I'm handing over Chase's $20 IOU. In modern times, this isn't a problem; stores know that Chase is good for the money and is backed by the FDIC.

In contrast, in the "Free Banking Era" of the mid-19th Century, there was not so much trust. The trustworthiness of bank deposits was "information-sensitive," in that the value of an IOU depended on specific facts about the bank's solvency (and existence). For example, the Bank of Boston might only give you $15 in exchange for a $20 note from the Bank of New York. This forced banks to constantly update books about the value of other banks' notes in their localities.

So, while I'm spending Chase's IOU as "money," Chase lends the "actual" $20 to somebody else, who deposits it in their Wells Fargo bank account in exchange for a $20 Wells Fargo IOU. Wells Fargo lends it to somebody else, who deposits it in their Bank of America account. Etc. And the game of "hot potato" continues. Even though we started with a $20 "monetary base," the fractional-reserve banking system and our acceptance of bank IOUs as "money" allows banks to "create" a much larger "money supply."

The (Long, Drawn-Out) End of the Gold Standard

The U.S. left the gold standard in 1934, and the Roosevelt administration made it illegal for private citizens to own gold. After World War II, the U.S., Great Britain, and the other major capitalist economies negotiated a new international monetary order, called the “Bretton Woods System.” Under Bretton Woods, the U.S. agreed to exchange dollars for gold at $35 an ounce, but the only entities allowed to make the exchange were other governments and central banks. In effect, the major capitalist economies went to a “U.S. Dollar standard,” where currencies were defined in terms of dollars, and dollars were defined (in theory) in terms of gold.

To sustain the Bretton Woods system required ever-increasing levels of domestic and international financial regulation. In part, the Bretton Woods monetary system had an inherent dilemma. The size of the world’s economy tripled from 1950 to 1970. Demand for U.S. dollars increased rapidly. If the U.S. did not export dollars to keep up with the demand, the world economy would falter. (This is the problem with any fixed currency, from gold to Bitcoin. If more people are chasing the same amount of money, prices plummet and the economy enters a recession.) But, since the U.S. dollar was based on a fixed gold supply, too many dollars in circulation would undermine faith in the U.S. dollar — the foundation on which the whole system relied. By the end of 1970, the U.S. had $11 billion in gold reserves, and $50 billion of circulating currency, all supporting a money supply of over $600 billion.

In 1971, President Nixon ended the Bretton Woods system. It used to be that the $1 bill in your pocket meant that the government (theoretically) owed you 1/35 ounce of gold. In a post–gold standard, post–Bretton Woods era, what does it mean? The government does not owe you a dollar of gold, or a dollar of silver, or a dollar of anything. The dollar simply is, by fiat of the federal government.

What is Money, Really?

Ignore computers and coins for the moment, and assume that the entire monetary base is made up of paper bills. For the sake of easy numbers, say that there is $1 trillion in paper currency out in the world. How did it happen that there is $1 trillion in currency out there? How does the number change?

The answer is the Federal Reserve. The Federal Reserve is the entity that issues those bills, and it controls the money supply.

Say the economy is growing too slowly for policymakers at the Fed, so they decide to lower interest rates. The Fed does this through "open market operations"; it buys securities (usually Treasury debt) on the open market. Commercial banks sell the Fed $1 billion in Treasury debt, and in exchange the Fed hands the banks $1 billion in cash. Where did the Fed get the cash? In our paper-only world, it just printed it. That's the beauty of being a central bank; you can just print money when you need it. Now, there is $1.001 trillion in paper currency out in the world.

Now, imagine that instead of handing the banks physical bills, the Fed hands them "virtual" bills that they place in a "bank reserves" database at the Fed. So, now we have two types of money — $1000 billion in bills issued by the Fed, and another $1 billion in the Fed's electronic bank reserves.

How Much Money Is There?

At the end of 2007, there was a monetary base of about $850 billion. We were very close to our hypothetical paper-only economy; of this $850 billion, about $790 billion was in the form of paper bills, about $40 billion was in the form of coins, and another $20 billion was on deposit in reserve accounts with the Federal Reserve. At the time, the M2 money supply was $7.5 trillion. The game of "hot potato" meant that about nine people had a claim on each government "dollar."

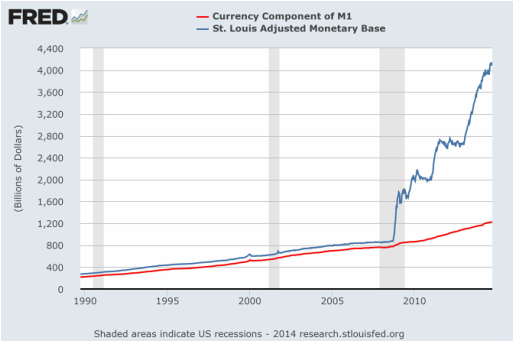

With the financial crisis of 2008, however, the world went crazy. With its Quantitative Easing programs, the Fed bought trillions of dollars of bank assets, inventing "database money" out of thin air and putting it on the ledgers of banks. Today, there is roughly $1.3 trillion of currency in circulation, but banks have another $2.8 trillion on reserve at the Fed. So there is a "monetary base" (MB) of $4.1 trillion, most of which exists only on computers. This increase in the monetary base is unprecedented.

Look at Figure 1 below. The blue line shows the monetary base over the last 25 years, and the red line shows the amount made up of hard currency. The difference between the two lines is the amount of "database money" sitting unused in banks' reserve accounts. You can see the three large jumps corresponding to QE1, QE2, and QE3.

Now, imagine that instead of handing the banks physical bills, the Fed hands them "virtual" bills that they place in a "bank reserves" database at the Fed. So, now we have two types of money — $1000 billion in bills issued by the Fed, and another $1 billion in the Fed's electronic bank reserves.

How Much Money Is There?

At the end of 2007, there was a monetary base of about $850 billion. We were very close to our hypothetical paper-only economy; of this $850 billion, about $790 billion was in the form of paper bills, about $40 billion was in the form of coins, and another $20 billion was on deposit in reserve accounts with the Federal Reserve. At the time, the M2 money supply was $7.5 trillion. The game of "hot potato" meant that about nine people had a claim on each government "dollar."

With the financial crisis of 2008, however, the world went crazy. With its Quantitative Easing programs, the Fed bought trillions of dollars of bank assets, inventing "database money" out of thin air and putting it on the ledgers of banks. Today, there is roughly $1.3 trillion of currency in circulation, but banks have another $2.8 trillion on reserve at the Fed. So there is a "monetary base" (MB) of $4.1 trillion, most of which exists only on computers. This increase in the monetary base is unprecedented.

Look at Figure 1 below. The blue line shows the monetary base over the last 25 years, and the red line shows the amount made up of hard currency. The difference between the two lines is the amount of "database money" sitting unused in banks' reserve accounts. You can see the three large jumps corresponding to QE1, QE2, and QE3.

Figure 1

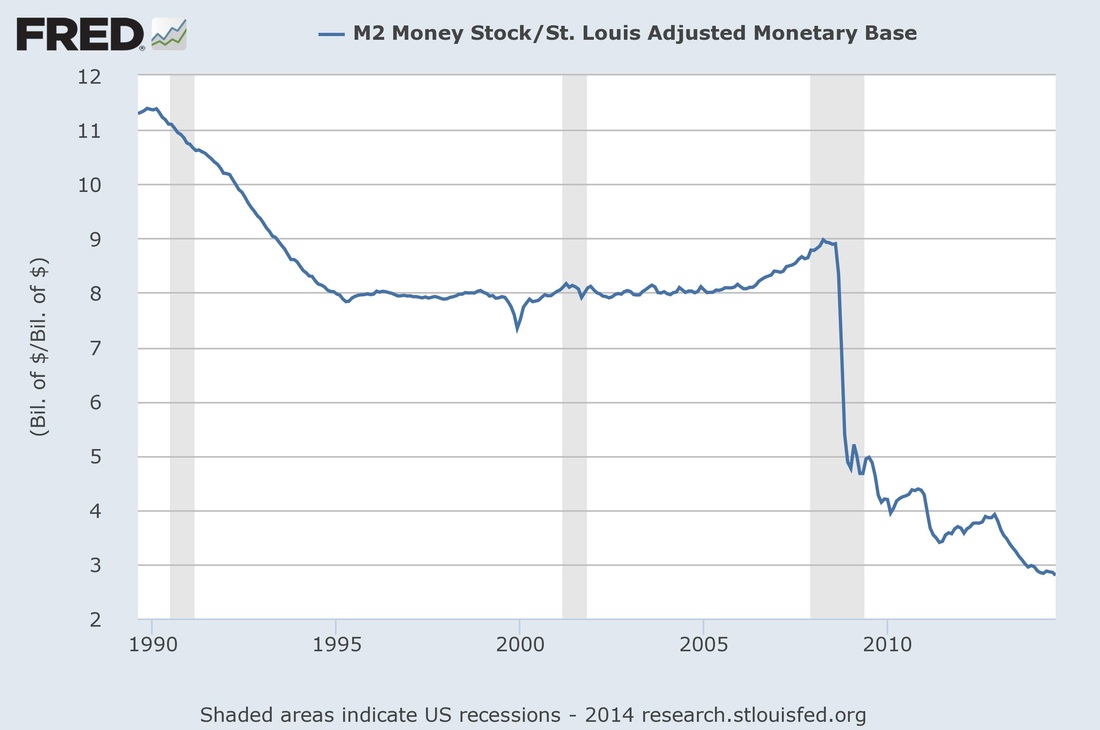

QE has not been as successful as hoped. Banks have not been lending that money out as fast as it has been created. In seven years, he monetary base has almost quintupled, but most of that money is not taking part in the game of "hot potato" that is economic activity. As a result, the M2 money supply has only gone up roughly 50 percent, to $11.5 trillion. Figure 2 shows the much steadier increase in M2, and Figure 3 shows the ratio of M2/MB.

Figure 2

|

Figure 3

|